Content

These are common questions I often get asked when I talk about depreciation when working with nonprofit organizations. Depreciation, a noncash expense is a well-known concept to trained accountants. But I’ve come to realize that it’s a concept that often creates confusion for those who are not involved in the weeds of accounting. At the end of the year, when Katie can better determine how much bad debt she needs to write off, she can adjust her allowance for doubtful accounts and her accounts receivable account accordingly. Any bad debt that she expenses for the year will be considered a non-cash expense because the amount is entered to reduce her accounts receivable balance and does not directly affect her cash balance. For small business owners, depreciation expenses are likely to be the most common type of non-cash expense that your business will need to worry about.

The two primary methods of accounting are the cash method and the accrual method. Before getting into the specifics of both the methods, it is important to note that depreciation is recorded only under the accrual system of accounting. There are numerous types of non-cash expenses your business may experience, but there are three non-cash charge examples that are most commonly experienced by small businesses. Depreciation is considered a non-cash expense since you’re only recording the monthly expense, as the cash outlay was already recorded when the item was originally purchased. Our online training provides access to the premier financial statements training taught by Joe Knight.

Noncash expenses must be recorded

In effect the noncash depreciation expense is added back because the depreciation expense had reduced the company’s net income reported on the income statement, but it did not use any cash during that period of time. The company records and recognizes non-cash expenses in its books of accounts under income statements. These expenses can be either paid in a previous financial year or accrue as expenses to be paid in the future. Non-cash expenses can also arise due to asset write-offs and other similar events. Such expenses reduce the amount of profits generated and have a negative impact on its profitability.

The meaning of depreciation per the Cambridge English Dictionary is that it is the process of losing value. Because you’ve already paid for the item in full when it was purchased, you’ll only be recording the item’s expense each month and not its cost. Financial Intelligence takes you through all the financial statements and financial jargon giving you the confidence to understand what it all means and why it matters. The way to balance this difference is to show the loss on the sale of a fixed asset as a sort of additional depreciation. This means that the amount shown as cash inflow is less than the net reduction in the value of fixed assets. Since analysts can’t use net income in a DCF model, they need to adjust net income for all the non-cash charges (and make other adjustments) to arrive at free cash flow.

What are non-cash expenses?

When going through the 7-Step process, it is important for the user to carefully read and understand the various intellitips which accompany each of the income statement and balance sheet entries in Steps 3, 4 and 5. These tips are accessible by hovering over the question mark to the left of each of the line items. Since the cash is received in Year 1, the entire amount is shown as revenues in Year 1. No expense https://kelleysbookkeeping.com/ is recorded since no cash has been paid for the expense, and hence this organization will show a net surplus of $250,000 in Year 1. In Year 2, the organization will record $100,000 as expenses, since Year 2 is when the cash is paid, and will have $0 revenues. When the cash flow statement is prepared under the indirect method, the net cash from operating activities is calculated by using the net income…

- Since analysts can’t use net income in a DCF model, they need to adjust net income for all the non-cash charges (and make other adjustments) to arrive at free cash flow.

- Noncash expenses are types of business expenses that are not paid in cash and are non-tangible that can include depreciation, amortization, bad debts, advertising costs, and research and development.

- While depreciation and amortization are the most common types of non-cash expenses your small business will likely need to deal with, there are several other types of non-cash expenses you should be aware of.

- The company records and recognizes non-cash expenses in its books of accounts under income statements.

- The most common example of a non-cash expense is depreciation, where the cost of an asset is spread out over time even though the cash expense occurred all at once.

- If the market price on the balance sheet date is higher than its purchase price, it’s a situation of unrealized gain.

Ask questions and participate in discussions as our trainers teach you how to read and understand your financial statements and financial position. Another example of a required adjustment is a loss on the sale of a fixed asset. A loss on the sale of a fixed asset is, in fact, a form of additional depreciation. Now that we have covered the technical aspects, let’s discuss how depreciation impacts cost recovery in your business model. The most critical step in creating a sound, financially sustainable business model is knowing the true cost or full cost of your programs. Allocating these costs over the useful life also means that the organization is not recording a huge expense of $515,000 in Year 1 which would result in skewing up the operational results in that year.

Create a Free Account and Ask Any Financial Question

A non-cash expense is an expense that is reported on the income statement of the current accounting period, but there was no related cash payment during the period. The most common example of a non-cash expense is depreciation – where the cost of an asset is spread out over time even though the cash expense occurred all at once. A fixed asset is often purchased for cash up front but the accounting recognition of the related expense is allocated over its useful life, e.g. 5 years, 7 years, etc. A non-cash charge is a write-down or accounting expense that does not involve a cash payment. They can represent meaningful changes to a company’s financial standing, weighing on earnings without affecting short-term capital in any way.

- However, these transactions do not impact the cash flow of the business but have a significant impact on the bottom line of the income statements, i.e.reduces, the profits reported.

- Some of the more important ones include Depreciation, bad debts (impairment), and loss on disposal of Fixed Assets.

- Noncash expenses are expenses that do not result in the transfer of cash from the business’s bank account to another party.

- It can also be included as indirect cost allocable to the program, for instance, depreciation on property out of which the program is being implemented.

- In addition, an accrued expense may be recorded for which the related cash expenditure is in the following period.

- To arrive at the correct cash flow on account of profits, we must, therefore, add back non-cash expenses to the figure of net profit disclosed by the income statement.

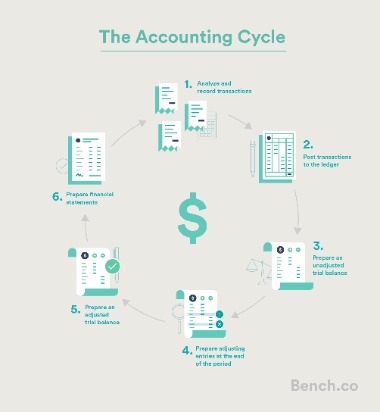

The Capitalization policy sets a threshold, above which expenditures are recorded as fixed assets (therefore should be depreciated) and below which are charged to expenses in the year that the expenses are incurred. Based on the management’s estimate that the useful life of the FFE is five years, the annual depreciation expense is $101,000. The allocation of the cost of the FFE over five years can be shown on a timeline as follows. Under the accrual method, revenues are recorded in the period in which it is earned (revenue recognition principle) and expenses are recorded in the same period in which the corresponding revenue is earned (matching principle). Under the cash method, revenue is recorded when cash is received, and expenses are recorded when cash is paid.

Such charges are often the result of changes to accounting policy, corporate restructuring, the changing market value of assets or updated assumptions on realizable future cash flows. The noncash items are subtracted from the income statement noncash expenses to prepare the cash flow statement. For example, accounts receivable is money that a business owes and has not received. In business accounting, non-cash transactions include any items that do not directly involve the transfer of money.