If the company has made huge progress, they will record the revenue base on the actual result as well. If the outcome of a contract cannot be estimated reliably, then no profit should be recognized. This is because recognizing profit would give a misleading picture of the contract’s true financial status. Instead, contract revenue should only be recognized to the extent that contract costs are expected to be recoverable.

This method involves estimating the percentage of work that has been completed at the end of each reporting period and then recognizing that amount of revenue and expense. Sometimes, this work may not be complete when a company prepares its accounts. Therefore, the company must perform specific accounting treatments to present this work. The process is not complex but requires an understanding of the concept first.

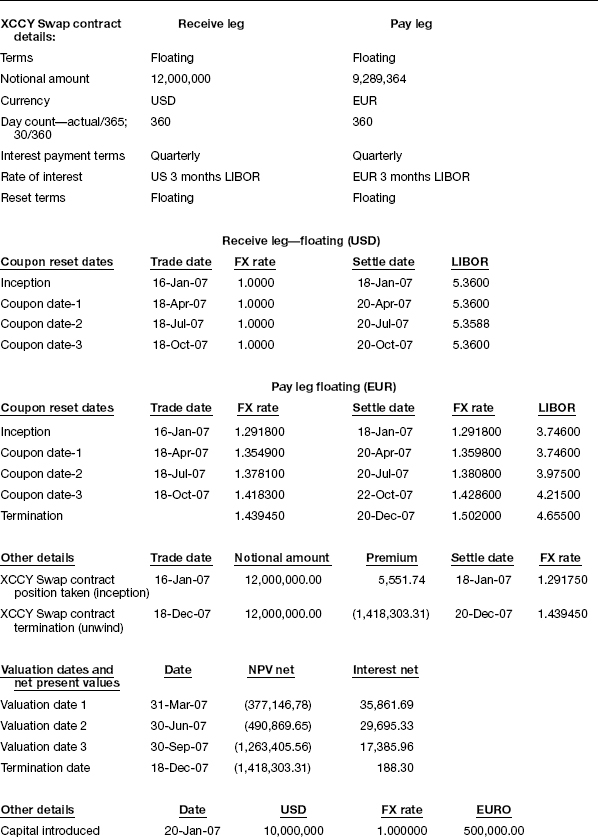

7 Schedule and Budget Updates

Companies overbill to help offset the negative impact on cash flow caused by slow-paying customers (unfortunately a common occurrence in the construction industry). And of course, it’s always better to get your cash in hand sooner rather than later! A construction work-in-progress is recorded in a company’s balance sheet as a part of the PP&E, or property, plants, and equipment account.

- Under

the “completed-contract” method, the entire profit of $100,000 would be

reported in year 3. - Consequently, the

scheduling process should be readily available as the project is underway. - The CIP report includes a detailed account of ongoing costs, including labor, materials, and overhead.

Retainage amounts are often substantial, amounting to 5% to 10% of the contract value. This emphasizes the fact that accurately accounting for all costs is key to determining whether projects make a profit, break even or lose money. Determining whether construction projects will be profitable is more difficult than in industries such as retailing or manufacturing, due to all of the factors above. Each project brings its own unique challenges, while change orders and fluctuating expenses during projects further complicate the picture. Construction costs should be recorded by debiting construction in process and crediting the cash account, and if the amount is still due, accounts payable should be credited. Classifying a CWIP as a current asset can help to provide businesses with an accurate representation of their financial health.

The overall status of the project requires synthesizing the different pieces of

information summarized in Table 12-8. Each of the different accounting systems

contributing to this table provides a different view of the status of the project. In this

example, the budget information indicates that costs are higher than expected, which could

be troubling.

Revenue recognition

While items 1 through 3 are actual figures, the 4th point (estimated cost to complete) requires strong job costing and estimating to determine. Ensuring this figure is as accurate as possible will avoid surprises when jobs finish. WIP is a concept used to describe the flow of manufacturing costs from one area Construction in progress accounting of production to the next, and the balance in WIP represents all production costs incurred for partially completed goods. Production costs include raw materials, labor used in making goods, and allocated overhead. Working capital turnover measures how much revenue each dollar of working capital is producing.

Most of these challenges arise from the fact that construction is project-based, and each project involves unique problems and solutions. Consequently, the

scheduling process should be readily available as the project is underway. Where the cost per work unit (ct) is replaced by the time per unit, ht, divided

by the cost per unit of time, ut. Failing to scrutinize contracts for unacceptable penalties and conditions can lead to loss-making projects, customer disputes or even lawsuits. In the dynamic and multifaceted realm of construction, these specialized financial statements play a pivotal role. They not only ensure precise financial tracking but also underpin the strategic decision-making essential for the sustained success of construction entities.

Balance sheets

Most of the time, company record the expense base on the actual cost and they use the cost estimate as the percentage of completion. With construction companies always on the move, there are more categories and accounts to keep track of, creating challenges that are unique to the construction industry. One of these challenges is learning how to record construction in progress accounting.

The WIP figure reflects only the value of those products in some intermediate production stages. This excludes the value of raw materials not yet incorporated into an item for sale. The WIP figure also excludes the value of finished products being held as inventory in anticipation of future sales.

Free Financial Statements Cheat Sheet

We used the unbilled accounts receivable account to prevent confusion with the bill receivable which represents the amount we already bill to customers. Two assets are considered as one contract unless they are negotiated as a single deal. For instance, if a cement manufacturing company is expanding the manufacturing unit. It will use cement from its own inventory, therefore, debiting the inventory account. Tight deadlines and thin profits mean you can’t afford errors or delays in construction WIP reports.

Another objective of recording construction in progress is scrutiny and audit of accounts. The construction in progress can be the largest fixed asset account due to the possibility of time it can stay open. Therefore, the construction in progress is a non-current asset account that keeps a record of all the costs incurred until completion.

As such, the difference between WIP and finished goods is based on an inventory’s stage of completion relative to its total inventory. WIP and finished goods refer to the intermediary and final stages of an inventory life cycle, respectively. A business with a quick ratio above 1 is regarded as liquid, meaning that it has enough cash resources to pay its current liabilities. Conversely, a business with a quick ratio below 1 does not have enough cash resources, so it will need to get an influx of cash through financing or by selling other long-term assets. Whether you are the one withholding retainage or it is withheld from your payments, accounting for retainage requires an addition to the chart of accounts. Retainage doesn’t belong in accounts receivable or payable, because it is not collectible (or payable) until the contract conditions have been met for its release.

WIP Example

A monthly balance sheet is crucial for a construction business to keep track of its financial health, and a balance sheet produced at the end of the fiscal year provides a compelling look at year-over-year growth. Even when they are not collectible within the “current” timeframe of 12 months, retainage accounts are typically shown as current accounts and current liabilities, respectively. As a result, the financial statements of construction companies often include a paragraph describing the special treatment of retention. By the time a company using cash accounting recognizes a cash flow problem, it’s often too late to do anything about it.

The terms work-in-progress and finished goods are relative terms made in reference to the specific company accounting for its inventory. It’s incorrect to assume that finished goods for one company would also be classified as finished goods for another company. For example, sheet plywood may be a finished good for a lumber mill because it’s ready for sale, but that same plywood is considered raw material for an industrial cabinet manufacturer. For some, work-in-process refers to products that move from raw materials to finished products in a short period.

Architectural or Design Company Tax Breaks

For cash flow planning

purposes, a graph or report similar to that shown in Figure 12-3 can be constructed to

compare actual expenditures to planned expenditures at any time. This process of

re-scheduling to indicate the schedule adherence is only one of many instances in which

schedule and budget updating may be appropriate, as discussed in the next section. As a result, complementary procedures to those used in traditional financial accounting

are required to accomplish effective project control, as described in the preceding and

following sections. While financial statements provide consistent and essential

information on the condition of an entire organization, they need considerable

interpretation and supplementation to be useful for project management. Construction accountants manage, analyze and update a construction firm’s financial information.

Workers and equipment move from site to site, so firms must be able to account for the costs of travel and moving and installing equipment. Unlike companies in other industries, such as retail or manufacturing, construction accounting typically focuses on custom projects, each of which must be managed for profitability. Revenue should be recognized based on a percentage of completion, and to record, the revenue recognition construction in process should be debited, and construction revenue should be credited. Overbilling occurs when a contractor bills for contracted labor and materials prior to that work actually being completed. Company can use this percentage to estimate the work completion and record the revenue. If it is an old project from prior years, we need to exclude the cost that incurs in previous years.

Subtracting the earned revenue to date ($100,000) from the amount billed ($600,000) minus cost to date ($400,000) leaves a value of positive $100,000. Harold Averkamp (CPA, MBA) has worked as a university accounting instructor, accountant, and consultant for more than 25 years. If you’ve recently applied for and had your construction business loan denied, you may be wondering what to do next. Equity, also referred to as net worth, is made up of the assets left over after liabilities are paid. This equity may be held by the owner or shareholders depending on the business structure. Cash accounting is the simplest and most straightforward approach to tracking finances, but it’s also the most limiting.

In most cases, the credit will be account payable or cash if paid immediately. It relates to using that raw material in building the asset which is sold by the business as its normal operation. It is an accounting term used to represent all the costs incurred in building a fixed asset.

How Much Does It Cost to Build a Cabin? – Bob Vila

How Much Does It Cost to Build a Cabin?.

Posted: Tue, 25 Jul 2023 07:00:00 GMT [source]

Construction businesses record their revenues based on the accounting method that they use. For example, a company using the accrual method will note revenues based on billed payments even if they have not actually received payment. One potential downside of the percentage of completion method is that businesses may incidentally underpay or overpay for taxes depending on how accurately they estimate costs. Companies that underpay taxes must pay interest to the IRS on the amount underpaid, while companies that overpay will receive a return with interest — which is usually not as valuable as having cash on hand. The percentage of completion method has numerous advantages for companies that are balancing several long-term projects. Most importantly, this method enables financial managers to get a clear view of the current financial status of each project as well as the financial horizon as each project progresses.